For years we’ve been tracking college costs and adjusting them for inflation. See Education and Tuition Inflation for more information. During that time, I’ve repeatedly said that one of the primary drivers of increased education costs was the ease of getting a loan. Unfortunately, the vast majority of college freshmen see a loan as “free money” and don’t seem to understand the difference between a “Loan” and a “Grant”. And apparently, this past week, many college loans effectively became grants.

Looking at it from a different perspective, we might wonder what lessons former college students will learn from this largess. Will they determine that debt is good? Or perhaps, they will surmise that no matter how stupid their decisions are, (i.e. worthless degrees), the government will always bail them out. Today’s article comes from the halls of Academia but doesn’t praise the government’s philanthropy as you might expect. ~Tim McMahon, editor

Biden’s College Loan Forgiveness Program Will Raise College Costs

When I interviewed for a teaching job at a private college in Alabama more than twenty years ago, the recently elected governor had won partly on a platform in which the state would install a lottery system that would give students a $3,000 grant for college. As the provost and I discussed the prospects of this new program, he smiled and said, “We hope this lottery passes. Then we can raise tuition by $3,000.”

(The Alabama legislature, despite being controlled at the time by members of the governor’s party, failed to pass and implement the lottery.)

In the aftermath of President Joe Biden’s announcement that the government will forgive up to $20,000 of student loan debt for qualifying borrowers, the responses are following the political ideology of the commentators. For example, columnist Tressie McMillan Cottom of the New York Times declared it a “win,” although she then demanded even more loan forgiveness.

Betsy DeVos, who was secretary of education under Donald Trump, took the opposite position, declaring the loan forgiveness to be “illegal.” Responses elsewhere ranged from comparing Biden’s loan forgiveness program to Jesus Christ dying for the sins of the world and the loan forgiveness during the year of jubilee outlined in the Hebrew scriptures to the entire program being little more than a wealth transfer to those fortunate to go to college from those who didn’t have that privilege.

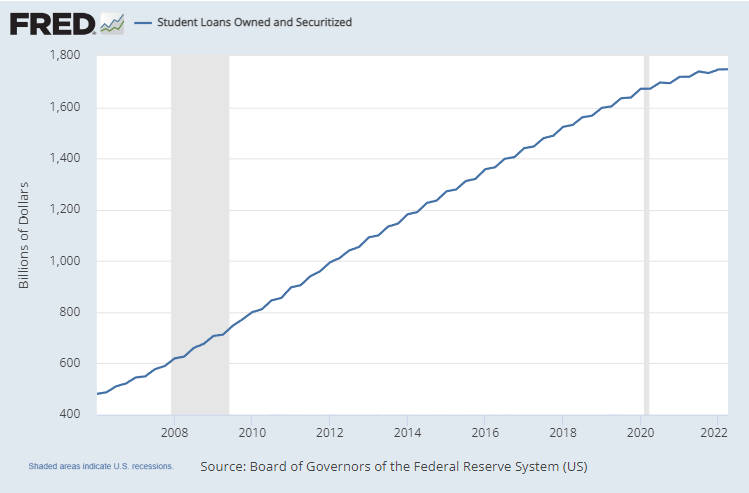

College Loans Have Helped Drive Up Higher Education Costs

While government officials are implying this is a one-time thing, we know that the political system will not put this to rest. After all, the forgiveness is being applied to student loans taken out in the past, yet college students continue to take out new loans for the coming academic year—and beyond. In fact, Biden’s loan forgiveness is going to have the same effect that my interviewer hoped would be the case if Alabama implemented a state lottery: higher prices for a college education.

That higher education costs have skyrocketed is a given. As Forbes explains:

In 1980, the price to attend a four-year college full-time was $10,231 annually—including tuition, fees, room and board, and adjusted for inflation—according to the National Center for Education Statistics. By 2019–20, the total price increased to $28,775. That’s a 180% increase.

Why tuition and fees have exploded is no mystery. On the supply side, college administrations have grown alongside federal mandates tied to identity politics. This development has had twofold effects. The first is to increase overall college costs—even though administrations have little to do with academic achievement. The second has been to increase the power and influence of the identity studies faculty, which is having a devastating impact upon higher education as a whole.

However, nonessential to a college education, administrative growth would not be possible without the government’s education loan programs, which are to increased costs what gasoline is to spreading a fire. When the Barack Obama administration in 2010 completely nationalized the student loan program, student loans outstanding stood at about $800 billion. Twelve years later, the amount has more than doubled to nearly $1.8 trillion. (One doubts that the value of a college education has more than doubled during the same time.)

To put it another way, student borrowers have financed the slow destruction of higher education, all the while placing enormous debts upon themselves. In the meantime, college administrators and faculty have seen their financial fortunes increase. When one adds politics into the mix, things become even more interesting.

Bending the Law to Reward Democratic Voters

There is no doubt that the student loan program mostly benefits people who vote Democratic. First, college administrators and faculty overwhelmingly lean Democratic, and college graduates are one of the most important Democratic Party constituencies, as well as the main beneficiaries of Biden’s executive order.

Furthermore, one doubts that this is the end of Biden’s loan forgiveness initiatives. Students that now are borrowing money to finance their college educations are tomorrow’s Democratic voters, and one doubts that their party will abandon them, especially when it can transfer their indebtedness (at least in part) to Republican taxpayers.

Perhaps one tweet says it all, this from Harvard Law School professor Laurence Tribe, who declared: “Good news for thousands of my former students. I’m grateful on their behalf, Mr. President.”

It is not an exaggeration to say that Harvard Law graduates are among the elite of the elites in what one might call our “ruling class,” and one doubts seriously that a president who already has demonstrated little restraint when it comes to fiscal matters suddenly will channel his inner Scrooge. Moreover, by employing what only can be called a twisted interpretation of an obscure law to announce loan forgiveness, Biden already has channeled another president known for his reckless policies, Franklin D. Roosevelt. David French writes:

the alleged legal basis for Biden’s $500 billion plan is found in a novel reading of the post 9/11 HEROES Act, which does grant the secretary of education broad authority to “waive or modify any statutory or regulatory provision applicable to the student financial assistance programs under title IV of the [Higher Education Act] … as the Secretary deems necessary in connection with a war or other military operation or national emergency.”

But even if one accepts the dubious proposition that this language includes the ability to waive payment entirely, the Biden administration would still have to show that the covid emergency justifies the action.

Like Roosevelt, who used the 1917 Trading with the Enemy Act to justify his gold seizure in 1933, Biden has used a little-known law to transfer wealth from those will little political influence to people who make the rules (but do not have obey them). It doesn’t matter that the language of the law has nothing to do with the president’s actions. Instead, it is the application of raw political power.

Conclusion

This is only the beginning of Biden’s financial shenanigans to benefit his party’s constituencies. Economist Alex Tabarrok has laid out ways that both higher education officials and students can further game Biden’s scheme. Regarding the real wealth transfers involved, French writes:

one of the fundamental flaws of the Biden plan is that it doesn’t just help those who need help. Instead, it imposes costs on those who need help to provide a substantial benefit to thousands upon thousands of college and graduate school graduates who don’t.

Understand that Biden invoked emergency powers to deal with something that under no circumstances counts as a crisis to transfer wealth from people with little political influence to those who are in or moving into the corridors of power. As the federal government continues to expand its reach—thus, making a college degree an even more vital gateway to better-paying occupations—the politically powerful will find more ways to dump their financial burdens upon those that can least afford them.

You might also like:

- Education and Tuition Inflation

- How Insidious Inflation Affects the Affordability of Tuition and Fees

- 8 Steps to Cut Education Costs

- Kids Going to College? Ease the Financial Burden

- Online Degree More Affordable Than on Campus

- Cutting the Cost of College

About the Author:

William L. Anderson is a retired professor of economics at Frostburg State University. He earned his MA in economics from Clemson University and his Ph.D. in economics from Auburn University.

William L. Anderson is a retired professor of economics at Frostburg State University. He earned his MA in economics from Clemson University and his Ph.D. in economics from Auburn University.

This article originally appeared here and has been reprinted under the creative commons license.